The Superannuation law requires that Trustees of all SMSF's formulate an investment strategy, regularly review that strategy, and give effect to the strategy whilst administering their SMSF. Each SMSF is unique to the members within that SMSF and accordingly the investment strategy must be unique in that it considers the particular circumstances of those members.

Whilst the ATO does not have a prescribed format for the investment strategy, the following factors must be considered.

- The Trustees objectives and cash flow requirements.

- The risk of undertaking, holding and realising investments of the SMSF.

- The likely return on the investments.

- The diversity or composition of the investments of the SMSF, is the SMSF adequately diversified to limit exposure to risks of singular asset classes.

- The liquidity of the investments in light of the SMSF's cash flow requirements.

- The ability of the SMSF to meet current and prospective cash flow requirements.

- Whether insurance for members of the SMSF should be held.

Investment strategies are not difficult to formulate if you ensure you have considered all the above. Whilst there is no legal requirement to have the investment strategy in writing it is difficult to prove it exists, has been considered, reviewed and complied with if it is not written down. The ATO and the SMSF auditor are interested in evidence of your active consideration and involvement of the above points. They are not prescriptive in what you decide or choose, just that you actively considered your choices and decisions.

The following steps will assist you in arriving at a compliant investment strategy:

- Consider YOUR SMSF's circumstances

Make sure your strategy considers your circumstances and the circumstances of other members. Things to be considered are overall risk profile (do the members understand the risk of the investment types held), age of the members, what investments and assets the members hold outside of the SMSF, the requirement for cash, the pension status of the members and liquidity in the SMSF.

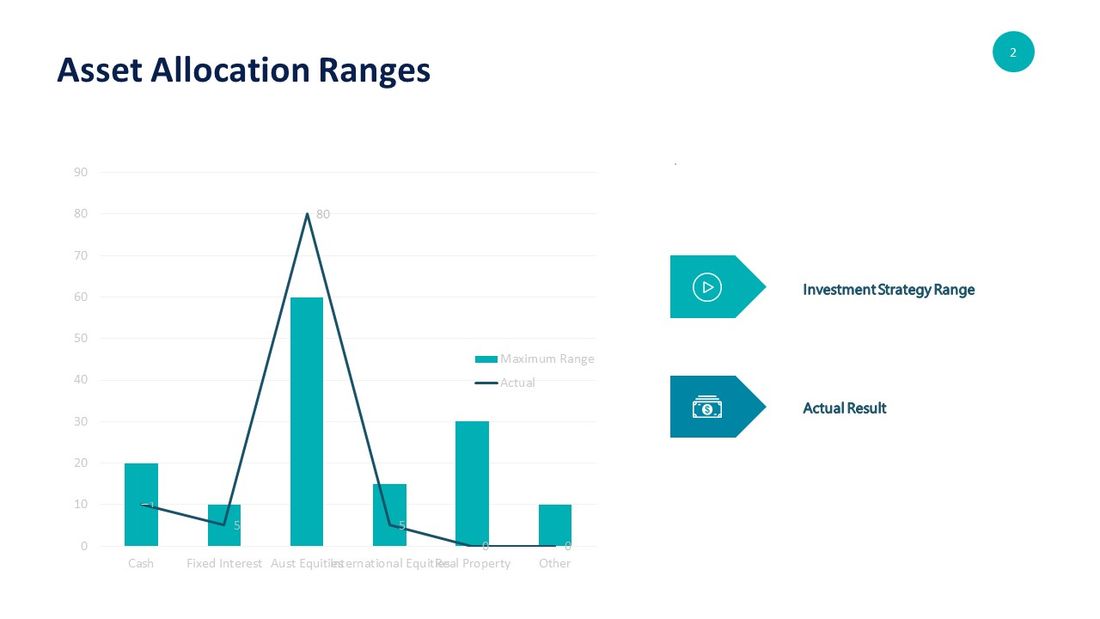

- Include asset allocation ranges

This demonstrates you have a strategy and that you have implemented your strategy.

- Make sure the ranges are appropriate

When establishing the ranges ensure they are broad enough to allow for normal market movements but not so wide that they cease to mean anything. A range of 0-100% for each asset class would render the asset allocations meaningless.

- Explain your diversification decisions

Your investments are not required by law to BE diversified; however, you are required to have considered diversification. Explain why you have invested in a specific investment or class of investments and the factors you considered in making that decision. If there is a lack of diversification you should acknowledge that you have considered the risks associated with the decision not to diversify and why you believe the potential returns will compensate for that risk.

- Explain your Liquidity Decision

When formulating the investment strategy, you must ensure that sufficient cash is available to meet the requirements of the SMSF.

Some of the things you should consider and comment on in documenting the liquidity decision are:

- What cash requirements the SMSF has for its regular operating expenses such as loan and investment commitments

- If there are changes to the amount of contributions due to a change in personal circumstances of the members how will that effect the SMSFs liquidity

- If the members commence pensions will the investments of the SMSF be sufficiently liquid to meet the annual minimum pension requirements or additional pension requirements if the member requests them

- If a member dies, how will the SMSF finance the payment of the death benefit. Are investments able to be transferred easily to the beneficiary of the SMSF if there is insufficient liquidity.

Note: This is of particular relevance to those drawing pensions where Real Estate is the primary investment of the SMSF.

- Don't set and Forget

Superannuation Law does require that you not only establish but also implement an investment strategy. Implementation includes review the strategy and whether your investments are made in accordance with the strategy. If for some reason the investments fall outside of the investment allocations, document that you have considered the occurrence and what actions you will take if any. It is ok for this to occur so long as you document any considerations and the resultant decisions regarding those investments.

- Review regularly

It is a requirement to review the investment strategy regularly to ensure it remains appropriate to the members objectives. This should be done at least annually. Major changes in the SMSF circumstances should also lead to a review. Examples of these circumstances include:

- Commencement or cessation of pensions

- Members join or leave the SMSF

- New classes of investments are made

- A member's circumstances or risk profile changes

- The SMSF enters an LRBA (Limited Recourse Borrowing Arrangement to fund the acquisition of investments)

Reviews should be documented in a minute or resolution that note the review and any changes to the Investment Strategy should be noted.

If you are unsure whether your Investment Strategy complies contact our office assistance or a copy of the ATO regulations.